The Unified Lending Interface (ULI): A Game-Changer for India’s Credit Landscape

- didoskeletonthough

- Jul 24, 2025

- 14 min read

Updated: Feb 16

Quote: "With ULI, your digital footprints become the key to opening doors of opportunity."

The Unified Lending Interface: A Game-Changer for India’s Credit Landscape

Unified Lending Interface (ULI) is a financial skeleton key—unlocking hidden opportunities for credit access while rattling the bones of traditional lending.

Introduced by the Reserve Bank of India (RBI), ULI is poised to transform how loans are processed, especially for underserved groups.

Topics:

What ULI is? whether it replaces or complements credit scores

How it works, its effectiveness in assessing creditworthiness for businesses, individuals, non-working people, and retirees

Its benefits, how India’s credit scoring compares to other countries

The future of this system.

An Example to understand ULI

Quote: "Unlock the strength of your financial skeleton—every smart choice builds a creditworthy future."

What is the Unified Lending Interface (ULI)?

The Unified Lending Interface (ULI), launched as a pilot in August 2023 by the RBI’s Innovation Hub, is a digital public infrastructure (DPI) platform designed to streamline loan processes in India.

You can think of it as the lending counterpart to the Unified Payments Interface (UPI), which revolutionized payments. ULI connects lenders (banks, NBFCs, fintechs) with borrowers and data providers through standardized APIs, enabling seamless, consent-based access to financial and non-financial data like land records, GST filings, utility payments, and milk cooperative data. It cuts paperwork, speeds up loan approvals, and enhances financial inclusion, particularly for rural borrowers, MSMEs, and those with limited credit history.

Quote: "With ULI, your digital footprints become the key to opening doors of opportunity."

Does ULI Replace or Complement Credit Scores?

ULI complements rather than replaces traditional credit scores (e.g., CIBIL, Experian, Equifax, CRIF High Mark, ranging from 300-900).

Credit scores rely on repayment history, credit utilization, and other financial metrics, but many Indians—especially rural farmers, MSMEs, and new-to-credit individuals—lack formal credit history, making them “un-bankable” under traditional systems.

ULI addresses this by using alternative data (e.g., utility bill payments, GST returns, land records, or milk pouring data) to assess creditworthiness, reducing dependency on credit scores.

For those with existing scores, ULI integrates credit bureau data alongside alternative sources, providing a fuller picture of creditworthiness. For example, a farmer with no CIBIL score but consistent UPI transactions and land records can be evaluated via ULI, while someone with a 750+ score benefits from faster approvals due to centralized data.

Quote: "A solid credit score is your shield—forge it with discipline and determination."

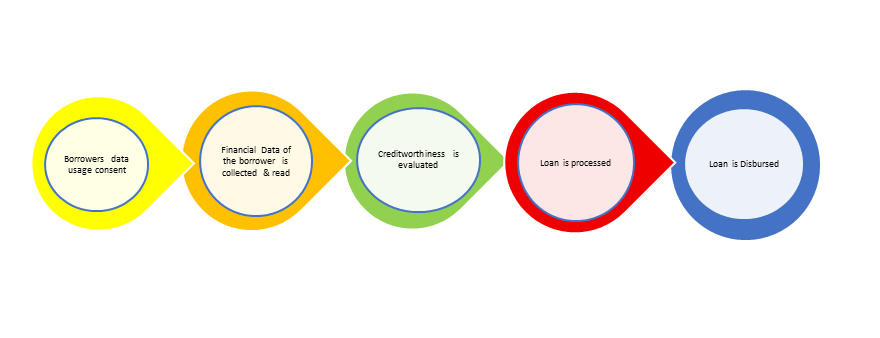

How Does ULI Work?

ULI operates as a plug-and-play platform with standardized APIs, connecting lenders to diverse data sources.

Here’s the process:

Borrower Consent: Borrowers grant permission for data access via Aadhaar e-KYC or DigiLocker.

Data Aggregation: ULI pulls financial (e.g., bank transactions, GST filings) and non-financial data (e.g., land records, satellite data, milk cooperative cash flows) from government, credit bureaus, and other providers.

Credit Assessment: Lenders use this data to evaluate creditworthiness, often with AI/ML to analyze patterns (e.g., a dairy farmer’s milk sales or a shop’s GST returns).

Loan Processing: Standardized APIs streamline verification, reducing loan approval times from weeks to minutes (e.g., Kisan Credit Card loans from 4-6 weeks to 10 minutes).

Disbursement: Loans are disbursed digitally, often without collateral, especially for small or rural borrowers.

ULI integrates with systems like Account Aggregators, DigiLocker, and government schemes (e.g., CGTMSE for MSMEs), ensuring compliance with RBI regulations and data privacy laws.

Quote: "Let ULI illuminate the shadows of your financial past and pave a path to prosperity."

Assessing Creditworthiness:

For Businesses, Individuals, Non-Working, and Retirees

ULI’s strength lies in its ability to evaluate diverse groups using alternative data, making it more inclusive than traditional credit scoring:

Businesses (MSMEs): MSMEs face a ₹20-25 trillion credit gap in India. ULI uses GST records, bank transactions, and even e-commerce sales (via ONDC) to assess cash flows, enabling loans for small businesses without formal credit history.

For example, a shopkeeper with consistent UPI sales can secure a working capital loan.

Individuals: For salaried or self-employed individuals, ULI combines credit scores with utility payments, mobile bills, or rental transactions, offering a broader view of financial discipline. This helps those with thin credit files (e.g., young professionals).

Non-Working Individuals: Unemployed or new-to-credit individuals benefit from ULI’s use of digital footprints (e.g., UPI transactions, utility bills). A homemaker with regular digital payments can prove creditworthiness without income proof.

Retirees: Retirees with pensions or fixed deposit interest can leverage ULI’s access to bank data or property records for loans (e.g., reverse mortgages). Their long credit history, combined with alternative data, ensures favorable terms, even without active income.

ULI’s data-driven approach makes it superior for underserved groups, as it doesn’t rely solely on traditional credit metrics, which often exclude non-working or retired individuals.

Quote: "Financial freedom begins when you master the art of creditworthiness."

Who Benefits from ULI and How?

ULI benefits the people across categories, cities, rural, anyone who needs to lend money for their life needs.

ULI’s inclusive design benefits multiple stakeholders:

Underserved Borrowers (Farmers, MSMEs, Rural/Informal Sector): Access to collateral-free loans, faster approvals (minutes vs. weeks), and lower interest rates due to better risk assessment.

For example, a dairy farmer’s milk cooperative data can secure a cattle loan in 10 minutes.

Lenders (Banks, NBFCs, Fintechs): Reduced operational costs, improved risk assessment via diverse data, and access to new customer segments (e.g., 120 million farmers, 80 million dairy farmers). Standardized APIs cut integration costs.

New-to-Credit Individuals/Retirees: Non-working or retired individuals gain loan access via digital footprints, bypassing traditional score barriers.

Economy: ULI addresses a $530 billion MSME credit gap and boosts agricultural lending (₹20 trillion disbursed by Jan 2024), supporting India’s $5 trillion economy goal by 2025.

Government: Enhanced financial inclusion aligns with RBI’s digital governance goals, reducing credit disparities in rural areas.

This is ULI’s potential to empower small businesses and rural borrowers, with some calling it a “UPI moment for credit.”

Quote: "With ULI, every transaction is a step toward a stronger, unseen financial backbone."

Comparing India’s Credit Scoring with Other Countries:

It is important to learn the systems used in other places and to understand how it different from ULI.

India’s credit scoring system, compared to global counterparts, has unique strengths and gaps:

India (CIBIL, Experian, Equifax, CRIF High Mark): Scores (300-900) rely on repayment history, utilization, credit mix, inquiries, and history length. Only 22% of Indians have a credit score due to low formal credit penetration.

ULI’s alternative data (GST, UPI, land records) aims to bridge this, targeting MSMEs and rural borrowers. Fortnightly bureau updates (RBI mandate since 2025) ensure real-time accuracy.

USA (FICO, VantageScore): Covers 90% of adults with scores (300-850), using similar metrics but with deeper data (e.g., utility payments, rental history).

Alternative data platforms like Experian Boost include non-traditional payments, similar to ULI. The US has faster credit reporting but less focus on rural inclusion.

China (Social Credit System): Combines financial and non-financial data (e.g., social behavior, bill payments) into a broad score, impacting loans, jobs, and travel.

Unlike ULI, it’s mandatory and government-controlled, raising privacy concerns. India’s consent-based ULI prioritizes user control.

UK (Experian, Equifax): Scores (0-999) use financial data and voter rolls. Alternative data is less prevalent, but open banking (like India’s Account Aggregator) allows real-time financial data sharing.

ULI’s broader non-financial data (e.g., satellite, milk data) is more innovative for rural lending.

Africa (M-Shwari, Tala): Mobile-based scoring uses call logs, mobile money transactions, and behavioral data, similar to ULI’s approach. These systems target unbanked populations but lack India’s scale and DPI integration (e.g., JAM, UPI).

India’s ULI stands out for its DPI integration and focus on underserved sectors, but its pilot stage (as of July 2025) lags behind the US’s mature systems. It surpasses China in privacy and rivals Africa in innovation for unbanked groups.

Quote: "Rise above financial doubts—your credit score reflects the power of your persistence."

Comparative Chart: Credit Scoring System – India vs USA vs China vs UK vs Africa

Feature / Country | 🇮🇳 India | 🇺🇸 USA | 🇨🇳 China | 🇬🇧 UK | 🌍 Africa (e.g., South Africa, Nigeria) |

Credit Score Range | 300 – 900 | 300 – 850 | 350 – 950 | 0 – 999 | 300 – 850 (varies by country) |

Main Credit Bureaus | CIBIL, Experian, CRIF, Equifax | Equifax, Experian, TransUnion | Baihang Credit, People's Bank of China (PBOC), Zhima Credit (Alipay) | Experian, Equifax, TransUnion | Compuscan (SA), CRC (Nigeria), CreditInfo |

Score Usage | Loans, credit cards, rental, jobs | Loans, mortgages, employment checks | Social credit pilot (behavioral) + credit loans | Loans, mortgages, car finance | Microloans, mobile lending, jobs |

Score Calculation Factors | Payment history, credit mix, duration, utilization, inquiries | Payment history, debt level, length, new credit, mix | Repayment, social behavior, online activity | Credit history, utilization, applications | Income history, mobile money usage, repayment |

Frequency of Updates | Monthly | Monthly | Varies (real-time in fintech apps) | Monthly | Monthly to quarterly |

Alternative Data Usage | Utility bills, rent data (in development) | Limited use | Yes (shopping, travel, fines) | Limited | Yes (telco, mobile transactions) |

Public/Private System | Mostly Private | Private Bureaus | State-run + Private | Private | Mix of private/public |

Availability to Users | Free once/year (official portals) | Free once/year | Limited access for users | Free once/year | Limited (growing in fintech apps) |

Fintech Integration | Moderate (growing with BNPL, UPI) | High | Very High (Alipay, WeChat Pay) | Moderate | High (mobile wallets, microfinance) |

Main Challenges | Low awareness, inconsistent updates | Data breaches, exclusions | Privacy concerns, overreach | Limited alt-data usage | Credit invisibility, fragmented data |

Key Takeaways:

India is formalizing with strong bureau coverage but needs awareness and alt-data inclusion.

USA has a mature system but struggles with exclusions and limited innovation in alt-data.

China blends credit and behavioral scoring, raising privacy alarms but boosting financial inclusion.

UK is similar to the USA, with high bureau use but needs better consumer control.

Africa (as a region) is innovating with mobile-based credit scoring via telco data due to lower formal credit history penetration.

Quote: "ULI is the bridge that connects your digital life to a world of lending possibilities."

The Future of the ULI System:

The future is bright for this system as the new data integration method will allow everyone to benefit.

ULI’s future is bright, with transformative potential:

Nationwide Rollout: After a successful pilot (e.g., Kisan Credit Card loans in 2023), ULI is set for a 2025-26 launch, expanding to personal, home, and MSME loans.

AI/ML Integration: Advanced analytics will refine credit assessments, predicting repayment ability via behavioral patterns (e.g., UPI spending trends).

New Data Sources: Integration of GST, customs, warehouse, and satellite data will deepen credit profiles, especially for MSMEs and farmers.

Credit Marketplace: ULI could evolve into a platform where borrowers compare loan offers, boosting competition and lowering rates.

Embedded Finance: Loans integrated into e-commerce or fintech apps (via ONDC, OCEN) will make borrowing seamless, like buying on EMI at checkout.

Data Privacy: Consent-based frameworks and compliance with India’s Digital Personal Data Protection Act will ensure secure data sharing.

Global Model: ULI could inspire other nations, combining UPI’s success with credit innovation.

Challenges include ensuring data privacy, training lenders on APIs, and scaling to India’s 1.4 billion population. Yet, with RBI’s backing and DPI like JAM-UPI, ULI could close the ₹20-25 trillion MSME credit gap and democratize credit, much like UPI did for payments.

Quote: "Your financial skeleton thrives when you turn challenges into creditworthy victories."

Takeaway:

ULI is a digital skeleton key, unlocking credit for India’s underserved—farmers, MSMEs, non-working individuals, and retirees—by complementing credit scores with alternative data.

Its plug-and-play APIs streamline lending, cutting approval times and costs while boosting inclusion.

Compared to the US, China, or Africa, India’s ULI blends innovation with scale, targeting rural gaps with DPI prowess. As it evolves with AI, new data, and embedded finance, ULI could redefine lending, making your financial skeleton not just visible but powerful.

Check your digital footprint—ULI might soon make it your ticket to credit.

Quote: "Creditworthiness is not a gift—it’s a legacy you create with every financial decision."

A Real-Life Example for Individuals:

Imagine a financial skeleton key that unlocks loans without the usual red tape—welcome to the Unified Lending Interface (ULI), India’s digital revolution in lending. ULI is like a cryptic puzzle, revealing creditworthiness through hidden data trails.

Let’s explore ULI through a detailed example of an individual, showing how it works, how it complements credit scores, its effectiveness for various groups, and who it benefits. We’ll also peek into its future, all while keeping it clear and engaging.

Meet Priya: An Example of ULI in Action

Priya, a 28-year-old freelance graphic designer in a small town in Gujarat, earns ₹20,000-30,000 monthly through irregular gigs. She has no formal credit history (no credit card or prior loans), so her CIBIL score is -1 (no score). She needs a ₹1 lakh loan to buy a new laptop and upgrade her home workspace to take on bigger projects. Traditional banks reject her due to her lack of credit history and irregular income.

Quote: "With ULI, even the smallest digital trail can lead to the treasure of financial approval."

Step-by-Step: Let us review how the system will work for her.

How ULI Helps Priya-

Loan Application and Consent:

Priya applies for a loan through a fintech app (e.g., SmartCoin, mentioned in your prior queries) partnered with ULI. She uses Aadhaar e-KYC & DigiLocker to give consent for data access, ensuring compliance with India’s Digital Personal Data Protection Act.

Data Aggregation via ULI:

ULI’s standardized APIs connect to multiple data sources to build Priya’s financial profile:

UPI Transactions: Priya’s PhonePe account shows consistent ₹15,000-20,000 monthly inflows from clients and regular bill payments (electricity, mobile).

Utility Bills: Her electricity and internet bills, paid digitally, reflect timely payments over 18 months.

GST Records: Priya recently registered for GST as a freelancer, showing ₹2.5 lakh in annual revenue.

Bank Account Data: Her savings account (via Account Aggregator) shows ₹50,000 in average balance and no overdrafts.

Alternative Data: ULI pulls her rental payment history (via a digital platform) and local cooperative society records, confirming her reliability.

Unlike traditional systems, ULI doesn’t rely solely on a credit score, which Priya lacks. Instead, it creates a holistic profile using her digital footprint.

Credit Assessment:

The lender’s AI/ML algorithms, integrated with ULI, analyze Priya’s data:

Consistent UPI inflows suggest stable earnings, despite irregularity.

Timely bill and rent payments indicate financial discipline, akin to a 700+ credit score.

GST data confirms her business activity, boosting her loan eligibility.

The system assigns her a risk profile equivalent to a 720 CIBIL score, even without a formal score.

Loan Approval and Disbursement:

Within 15 minutes, Priya is approved for a ₹1 lakh personal loan at 12% interest (vs. 18% for high-risk borrowers). The lender uses ULI’s APIs to verify data instantly, bypassing weeks of paperwork. The loan is disbursed to her bank account via UPI, and she sets up auto-debit for EMIs.

Outcome:

Priya buys her laptop, takes on bigger projects, and repays the loan on time. Her repayment data is reported to CIBIL, building her credit score (starting at ~650 after six months). ULI’s seamless process turns her financial skeleton from invisible to vibrant.

Quote: "Creditworthiness is the heartbeat of your financial soul—nurture it with every payment."

Does ULI Replace or Complement Credit Scores?

In Priya’s case, ULI complements her non-existent credit score. Traditional bureaus (CIBIL, Experian, Equifax, CRIF High Mark) rely on credit history, which Priya lacks.

ULI fills this gap by using alternative data (UPI, bills, GST) to assess her creditworthiness. For those with scores, ULI enhances evaluations by adding non-financial data, ensuring faster and fairer lending.

For example, If Priya had a 600 score (below average), ULI’s data could justify a better loan offer by proving her reliability. Posts on X highlight ULI’s role in reducing credit bureau dependency for new-to-credit borrowers like Priya.

Quote: "With ULI, even the smallest digital trail can lead to the treasure of financial approval."

How ULI Assesses Creditworthiness Across Groups?

ULI’s strength is its inclusivity, tailoring assessments for diverse groups:

Individuals (like Priya): Freelancers or salaried workers with thin credit files benefit from ULI’s use of digital payments (UPI, bills) and bank data. It’s ideal for young professionals or urban gig workers.

Businesses (MSMEs): A small shopkeeper can use GST returns, e-commerce sales (via ONDC), or UPI transactions to prove cash flow, securing working capital loans without collateral.

Non-Working Individuals: Homemakers or unemployed individuals with digital footprints (e.g., utility payments, UPI transfers) can demonstrate reliability, accessing small loans.

Retirees: Those with pensions, fixed deposit interest, or property records (via ULI’s land data integration) can secure loans like reverse mortgages, even with limited income.

ULI outperforms traditional scoring for groups with sparse credit histories, as it leverages India’s digital infrastructure (JAM, UPI) to capture real-time behavior. For Priya, her lack of a score was no barrier—ULI’s data painted her as creditworthy.

Quote: "Shape your financial destiny—creditworthiness is the compass guiding your journey."

Who Benefits and How?

ULLI can benefit people across various categories. The system reduces bias across ones professional and personal lifestyle. The idea is to allow everyone to gain access to the lending system. It is designed for inclusiveness.

The example highlights ULI’s beneficiaries:

New-to-Credit Individuals: Access loans without formal credit history, enabling career growth or personal investments. Priya’s ₹1 lakh loan at 12% saved her ₹6,000 annually vs. high-interest alternatives.

Underserved Groups (Farmers, MSMEs): Rural borrowers or small businesses use non-traditional data (land records, milk cooperative payments, GST) for collateral-free loans, closing India’s ₹20-25 trillion credit gap.

Non-Working/Retirees: Digital footprints or pension data unlock credit, supporting medical or family needs without relying on employment.

Lenders: Banks and fintechs cut costs (e.g., 60% reduction in verification time) and reach untapped markets (120 million farmers, 80 million dairy farmers).

Economy: ULI boosts financial inclusion, supporting India’s $5 trillion economy goal by 2025, as seen in its pilot success (₹20 trillion in agricultural loans by Jan 2024).

Quote: "ULI empowers your financial skeleton to stand tall in the modern lending world."

Comparing ULI to Traditional Credit Scores:

Traditional credit scores (300-900) rely on repayment history (35%), credit utilization (30%), credit mix (10%), inquiries (10%), and account age (15%).

ULI’s edge is its broader data scope:

Traditional Scores (India): Limited to those with credit history (22% of Indians). Priya’s -1 score would exclude her from most loans.

ULI: Includes alternative data, making it accessible to 70%+ of Indians with digital footprints (e.g., 800 million UPI users). Priya’s UPI and GST data secured her loan.

Global Comparison (e.g., USA’s Experian Boost): Similar alternative data (utility, rent payments) but less focus on rural sectors. ULI’s integration with India’s DPI (Aadhaar, UPI) is unique.

Unified Lending Interface (ULI) vs Traditional Credit Rating System – India

Feature / System | 🟢 Unified Lending Interface (ULI) | 🔵 Traditional Credit Rating System |

Core Purpose | Real-time, inclusive credit decision system | Risk assessment based on historical credit behavior |

Governing Body | RBI (via Public Tech Platform for Frictionless Credit - PTPFC) | RBI-regulated credit bureaus (CIBIL, Equifax, Experian, CRIF) |

Technology Used | Open network protocols (India Stack, Account Aggregator, OCEN) | Centralized credit bureau scoring and reports |

Credit Assessment Basis | Real-time data: cash flow, GST, bank statements, eKYC | Historical repayment patterns, credit utilization, loan accounts |

Data Sources | DigiLocker, Aadhaar, GSTN, bank APIs, eKYC, account aggregators | Banks, NBFCs, utility payments, credit card companies |

User Profile Coverage | Focus on New-to-Credit, MSMEs, rural borrowers | Mostly salaried, urban, credit-active individuals |

Speed of Lending Decision | Instant or near real-time | Days to weeks, dependent on underwriting & verification |

Inclusiveness | Highly inclusive, alternative data used | Limited; excludes those without formal credit history |

Transparency | API-driven, borrower-consent-based visibility | Bureau-controlled; borrowers often unaware of changes |

Primary Users | Banks, NBFCs, Agri-fintechs, MSME lenders, Rural credit systems | Banks, NBFCs, Housing finance, Telecom, Insurance |

Limitations | Tech adoption barriers, early-stage evolution, privacy concerns | Outdated data, credit invisibility, score manipulation |

Example Use Case | Small business loan via UPI + GST + eKYC verification | Home loan eligibility based on 750+ CIBIL score |

The Future of ULI:

ULI, still in pilot as of July 2025, is set for a nationwide rollout by 2026:

Expanded Data: Will include satellite data for farm loans, e-commerce sales, and more, refining risk models.

AI-Driven Scoring: Advanced analytics will predict repayment patterns, making Priya’s future loans even faster.

Credit Marketplace: Borrowers like Priya could compare loan offers in real-time, lowering rates.

Global Influence: X posts suggest ULI could inspire DPIs worldwide, like UPI did for payments.

Challenges include ensuring data privacy and scaling APIs. However, with RBI’s backing, ULI could democratize credit, much like UPI transformed payments.

Quote: "With ULI as your ally, your financial story evolves from obscurity to opportunity."

Conclusion:

For Priya, ULI turned her invisible financial skeleton into a ticket for growth, bypassing traditional credit score barriers. By aggregating UPI, GST, and utility data, ULI empowers individuals, businesses, non-working people, and retirees, making lending faster and fairer. Its future—AI-driven, inclusive, and global—promises to reshape India’s credit landscape. Check your digital footprint; ULI might soon unlock your next loan.

Summary:

ULI is a next-gen, data-driven credit access system for India’s underserved, digitally-verifiable segments.

Traditional systems focus more on existing credit holders and lag in real-time adaptability.

Call to Action:

Tried a digital loan yet?

Curious how ULI could help you?

Explore your digital transactions (UPI, bills) and share your thoughts below.

Note: We share tips, not financial advice. Some links below are affiliates, meaning we might get a small commission if you sign up (at no extra cost to you!). This is for educational use only—please consult a professional before investing. This post includes affiliate links to products we recommend.

To Purchase Books and other materials on the subject

Amazon- https://bitli.in/V4w8LG3

Flipkart- https://fktr.in/xkw9Sox

Subscribe- didoskeletonthoughts@gmail.com for newsletters and latest updates.

Disclaimer: Please be aware that this article was generated with the assistance of AI. It may contain affiliate links, meaning if you make a purchase through these links, the site may earn a small commission at no extra cost to you. The product recommendations provided are based on the information available at the time of generation and should be considered suggestions. It is crucial to conduct your own thorough research, read reviews, and compare products from various sources before making any purchasing decisions. Your individual needs and circumstances may vary, and the recommendations in this article may not be suitable for everyone. Exercise caution and make informed choices when buying products.

Affiliate Links Disclaimer: This article may contain affiliate links, through which I may earn a commission from purchases. Clicking on these links won't affect your experience or the content's integrity. Your support through these links is appreciated and helps sustain the quality of the service. Please review the terms and conditions before making purchases.

Comments